What to Do When Your Parents Ask 'When Should We Start Taking Social Security?'

This one started with my parents. They're at the point where they have to decide when to start claiming Social Security, and every conversation about it went the same way: a lot of gut feeling, a napkin calculation, and no easy way to actually see the tradeoff. So I built a small calculator.

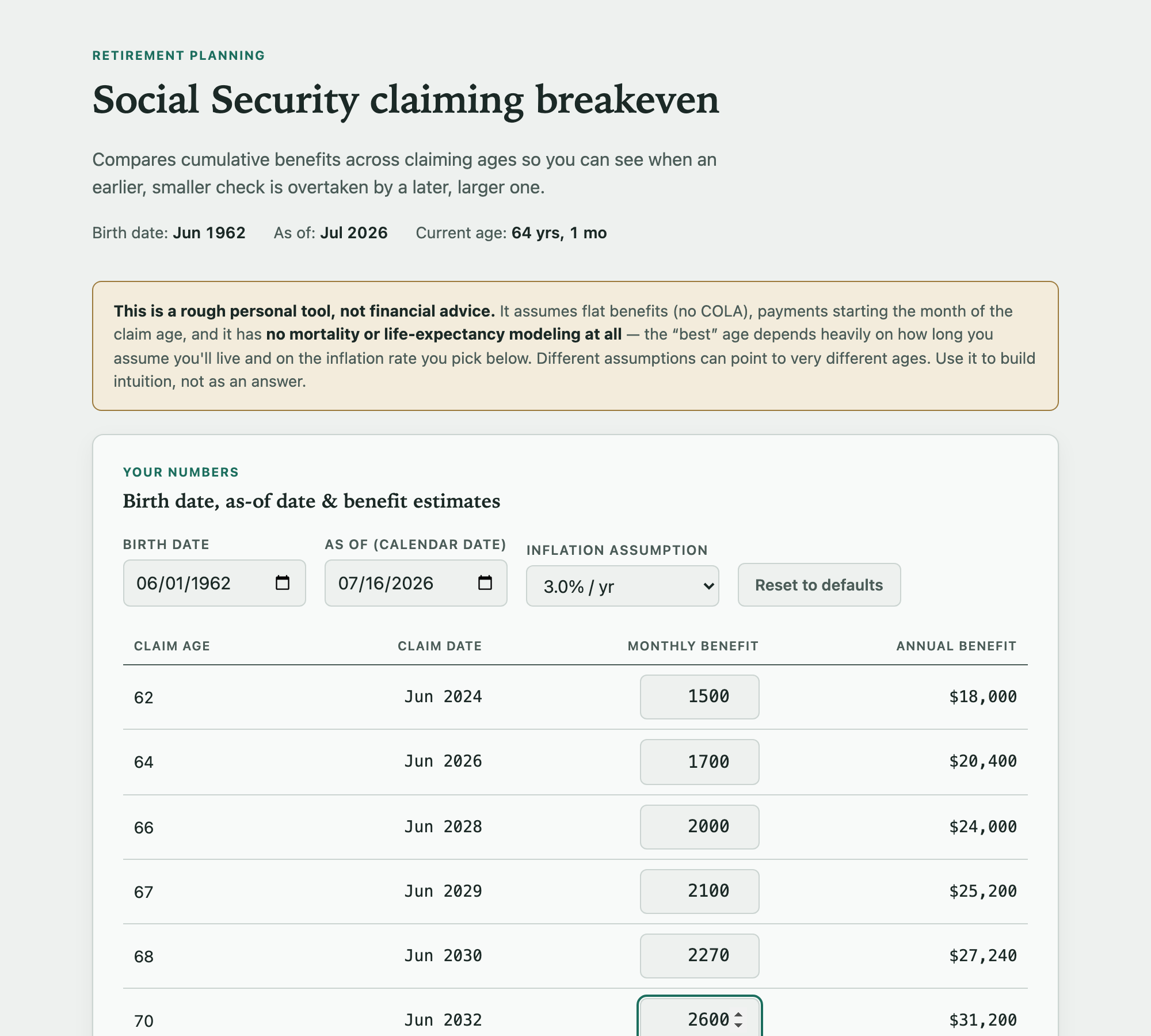

Try it here — it's a single page, no sign-up, nothing sent anywhere. You put in a birth date and your estimated monthly benefit at a few different claiming ages (that's on your my Social Security statement), and it shows you the "breakeven age" — the point where a later, bigger check has paid out more in total than an earlier, smaller one that had a head start. It does this in both nominal dollars and inflation-adjusted dollars, since a few percent of inflation compounded over 20+ years changes the picture a lot.

Here's the catch, and it's a big one: this is not an answer, it's a way to see the shape of the tradeoff. The calculator has no idea how long you're going to live. It just runs the math out to age 100+ and lets you eyeball where the lines cross. But the honest truth is that the "right" claiming age depends almost entirely on two guesses nobody can make with confidence — how long you'll actually live, and what inflation does over the next few decades. Nudge either one and a different age looks like the winner.

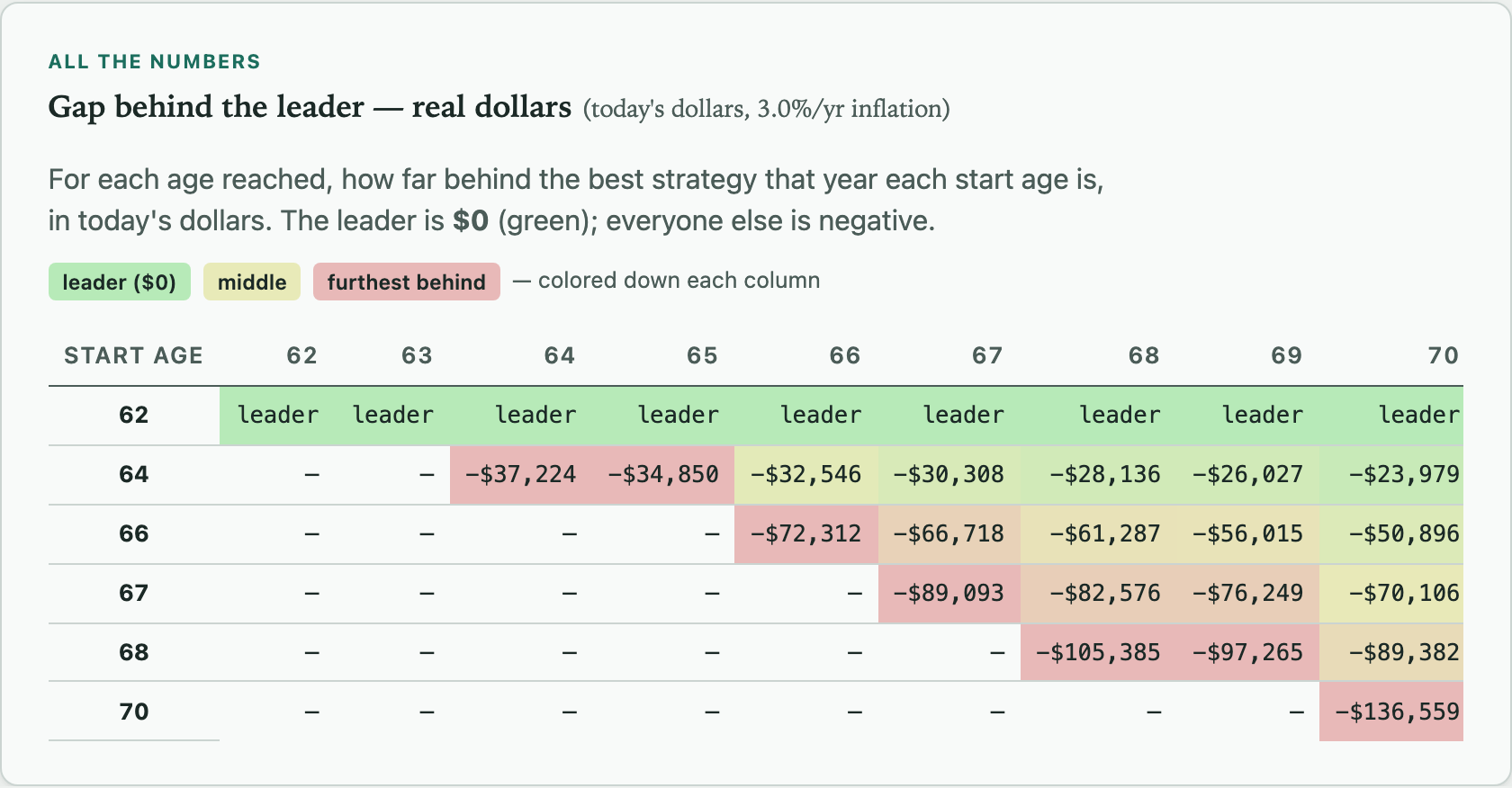

That's what the color-coded tables are for — green is whichever claiming age is winning at that point, red is how far behind everyone else is, in today's dollars. Watching the leader flip from green to red as you move across the columns is a more visceral way to feel the tradeoff than any single "breakeven age" number.

One thing that jumped out while playing with it: if you're not sure how long you'll live, and you're worried about picking the earliest age and dying rich, or picking the latest age and dying before it pays off, an option in the middle isn't a compromise so much as a hedge. It won't be the best outcome in any single scenario, but it shrinks how badly wrong you can be in either direction — which might matter more than chasing the theoretical optimum for a lifespan you can't actually know in advance.

If you want to poke at the numbers yourself, or see how it works, the code is on GitHub — it's a single HTML file, no build step, free to fork.